Ireland

Ireland

Since the US high yield fallen angels index was launched in 20051, this category has outperformed both the broad high yield and liquid high yield categories over every 5-year period on a rolling monthly basis.

Within the high yield market, fallen angels have:

|

*Fallen angels currently offer higher credit ratings

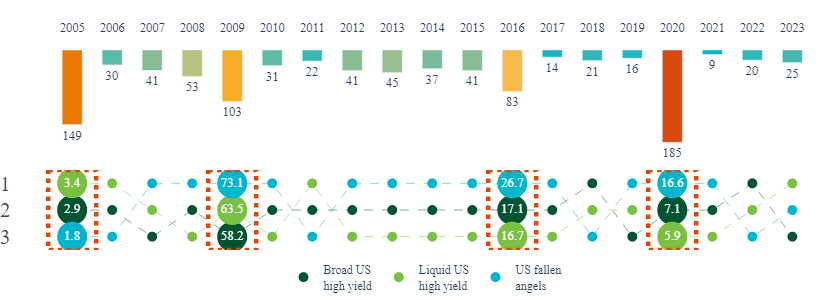

80% of the fallen angels index2 currently has a BB rating. This is higher than both the “broad high yield”2 and “liquid high yield"2 markets (Figure 1).

Figure 1: Fallen angels offer higher credit quality than broad high yield and liquid high yield indices1

*Fallen angels have offered higher total returns

Despite this, fallen angels have delivered higher returns than the broad high yield market. However, this does come with some additional volatility, which can be attributed to the lower level of diversification in fallen angels.

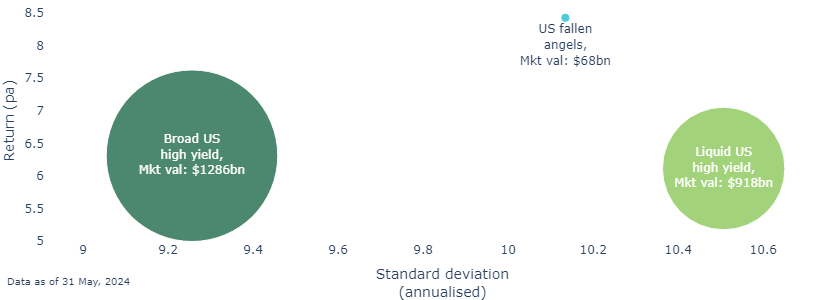

Fallen angels have also outperformed the liquid high yield index in both risk and return terms (Figure 2). This liquid high yield index is often the favoured index tracked by high yield ETFs. Fallen angels have outperformed the broad high yield and liquid high yield categories 100% of the time on a monthly rolling 5-year basis since the fallen angels index launched in 20051.

Figure 2: Fallen angels have delivered higher returns than the broad high yield market and higher risk-adjusted returns than the liquid high yield market2

**Fallen angels have historically outperformed during periods of rising rates

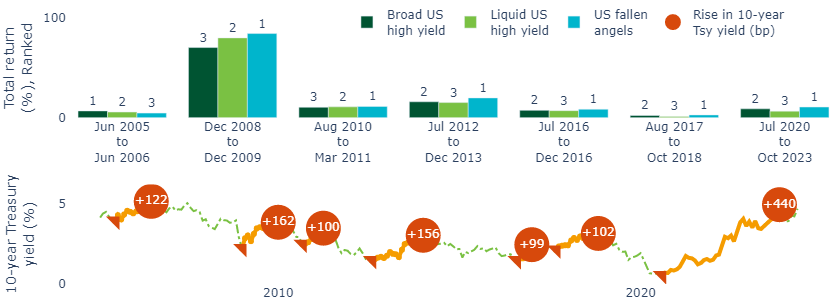

Although fallen angels are, on average, higher duration with greater sensitivity to interest rate changes, they have typically outperformed the broad and liquid high yield indices through the seven periods since 2004 where 10-year Treasury yields have risen by 1% or more (Figure 3).

Figure 3: Fallen angels have outperformed other high yield indices in rising rate environments, despite the additional duration sensitivity3

This is generally because rates tend to rise when the economy is improving. While fallen angels are impacted by rising yields, the positive contribution made by credit spread tightening at the same time has typically more than compensated for this.

Improving economic conditions have historically favoured fallen angels

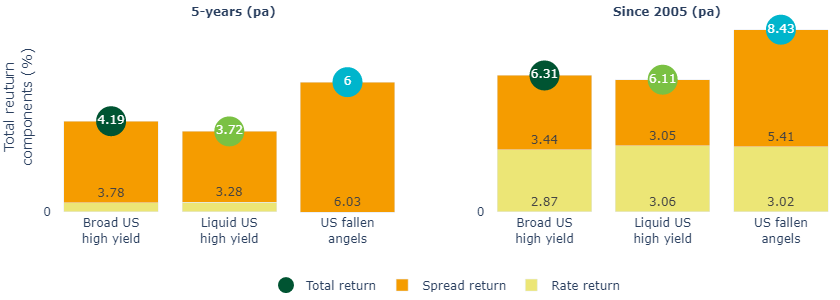

Fallen angels have historically seen stronger credit spread performance than the broad and liquid high yield markets over the last 5-years and since inception of the fallen angels index in 2005 (Figure 4).

Figure 4: Excess income over Treasuries and tightening credit spread has driven the relative outperformance of fallen angels4

***Fallen angels have outperformed broad high yield during high downgrade years

Historically, fallen angels have also outperformed the broad and liquid high yield markets during periods of high downgrade activity (Figure 5). During other periods, fallen angels have produced similar returns to the broad and liquid high yield markets.

Figure 5: Fallen angels have delivered solid performance through difficult markets4

We believe a strategic allocation to high yield reflecting an emphasis on fallen angels can reap rewards for long term investors

We believe that high yield credit offers value as a strategic allocation given the historical risk-adjusted returns exhibited in both benign and more challenging market conditions.

We also believe that an emphasis on fallen angels within this can enhance a high yield investment strategy, especially for investors able to access liquidity in this specialist fixed income sub-asset class.

Most read

Global macro, Fixed income

October 2023

Global macro research: Yield-curve inversion – an unreliable recession signal?

Global macro

July 2023

Global macro research: Asset allocation in focus

Global macro

May 2023

Global macro research: Why central banks may struggle to solve the inflation puzzle

Fixed income

August 2024